Pre-existing conditions (Uninsurable) clauses – exclusions

Pre-existing conditions (Uninsurable) clauses

The Pre X clause no longer applies to Individual or Group Health Insurance as it’s prohibited under Health Care Reform 45 CFR §147.108 and all coverage is GUARANTEED ISSUE §2701

Pre-existing condition exclusion means

a limitation or exclusion of benefits

In the past a Pre X clause (including a denial of coverage) was based on the fact that the condition – Medical Problem was present before covered began whether under a employer group health plan or individual health insurance coverage and often whether or not any medical advice, diagnosis, care, or treatment was recommended or received before that day. One needs to review the actual EOC Evidence of Coverage to know for sure.

A preexisting condition exclusion includes any limitation or exclusion of benefits (including a denial of coverage) applicable to an individual as a result of information relating to an individual’s health status before the individual’s effective date of coverage … such as a condition identified as a result of a pre-enrollment questionnaire – application or physical examination given to the individual, or review of medical records relating to the pre-enrollment period. 54.9801-2 Health Care Reform Facts Q 335

Here’s some 2024 figures on Medi Cal and other spending on various illnesses.

Obamacare PROHIBITS discrimination or

different rates based on health!

FAIR HEALTH INSURANCE PREMIUMS.

§2701 Page 37 HR 3590

‘‘(a) PROHIBITING DISCRIMINATORY PREMIUM RATES.—

‘‘(1) IN GENERAL.—With respect to the premium rate charged by a health insurance issuer for health insurance coverage offered in the individual or small group market—

(A) such rate shall vary with respect to the particular plan or coverage involved only by—

(i) whether such plan or coverage covers an individual or family;

(ii) rating area, [county – zip code] as established in accordance with paragraph (2);

Small Biz Rating Methods AB 1083

(iii) age, except that such rate shall not vary by more than 3 to 1 for adults (consistent with section 2707(c)); and

(iv) tobacco use, [Doesn’t apply in CA] except that such rate shall not vary by more than 1.5 to 1; and

(B) such rate shall not vary with respect to the particular plan or coverage involved by any other factor not described in subparagraph (A).

So does CA Law

A health insurer shall not establish rules for eligibility, including continued eligibility, of any individual to enroll under the terms of an individual health benefit plan based on any of the following factors:

(A) Health status.

(B) Medical condition, including physical and mental illnesses.

(C) Claims experience.

(D) Receipt of health care.

(E) Medical history.

(F) Genetic information.

(G) Evidence of insurability, including conditions arising out of acts of domestic violence.

(H) Disability.

(I) Any other health status-related factor as determined by any federal regulations, rules, or guidance issued pursuant to Section 2705 of the federal Public Health Service Act.

Underwriting Declinable Conditions Health Questions

Examples of Declinable Conditions Medical Underwriting Kff.org In the Medically Underwritten Individual Market, Before the Affordable Care Act – Group Market before AB 1672 1992 CA :

Condition Condition

AIDS/HIV Lupus

Alcohol abuse/ Drug abuse with recent treatment Mental disorders (severe, e.g. bipolar, eating disorder)

Alzheimer’s/dementia Multiple sclerosis

Arthritis (rheumatoid), fibromyalgia, other inflammatory joint disease Muscular dystrophy

Cancer within some period of time (e.g. 10 years, often other than basal skin cancer) Obesity, severe

Cerebral palsy Organ transplant

Congestive heart failure Paraplegia

Coronary artery/heart disease, bypass surgery Paralysis

Crohn’s disease/ ulcerative colitis Parkinson’s disease

Chronic obstructive pulmonary disease (COPD)/emphysema Pending surgery or hospitalization

Diabetes mellitus Pneumocystic pneumonia

Epilepsy Pregnancy or expectant parent

Hemophilia Sleep apnea

Hepatitis (Hep C) Stroke

Kidney disease, renal failure Transsexualism

Declinable Medications

Anti-Arthritic Medications

Adalimumab/Humira

Cyclosporine/Sandimmune

Methotrexate/Trexall

Ustekinumab/Stelara

others

Anti-Diabetic Medications

Avandia/Rosiglitazone

Glucagon

Humalog/Insulin products

Metformin HCL

others

Medications for HIV/AIDS or Hepatitis

Abacavir/Ziagen

Efavirenz/Atripla

Interferon

Lamivudine/Epivir

Ribavirin

Zidovudine/Retrovir

others

Anti-Cancer Medications

Anastrozole/Arimidex

Nolvadex/Tamoxifen

Femara

others

Anti-Psychotics, Autism, Other Central Nervous System Medications

Abilify/Ariprazole

Aricept/Donepezil

Clozapine/Clozaril

Haldol/Haldoperidol

Lithium

Requip/Ropinerole

Risperdal/Risperidone

Zyprexa

others

Anti-Coagulant/Anti-Thrombotic Medications

Clopidogrel/Plavix

Coumadin/Warfarin

Heparin

others

Miscellaneous Medications

Anginine (angina)

Clomid (fertility)

Epoetin/Epogen (anemia)

Genotropin (growth hormone)

Remicade (arthritis, ulcerative colitis)

Xyrem (narcolepsy)

others

Jump to section on:

Medi Gap

ACA/Health Care Reform

All our plans are Guaranteed Issue with No Pre X Clause

Quote & Subsidy #Calculation

There is No charge for our complementary services

Watch our 10 minute VIDEO

that explains everything about getting a quote

- Our Quote Engine Takes all the complexity out of using pencil and paper to figure out the premiums per the Obamacare/ACA rules under CFR §1.36B-3 *

- Get more detail on the Individual & Family Carriers available in CA

Pre X in Medi Gap?

When might there be a Pre-X clause in #Medi-Gap for California Policies

Maybe if there is Medical Underwriting. ACA/Health Care Reform didn’t change the rules for Medi Gap. No pre-x if you enroll during a guaranteed issue time.

Guaranteed issue rights (also called “Medigap protections”)— Rights you have in certain situations when insurance companies are required by law to sell or offer you a Medigap policy. In these situations, an insurance company can’t deny you a Medigap policy, or place conditions on a Medigap policy, like exclusions for preexisting conditions, and can’t charge you more for a Medigap policy because of a past or present health problem. Publication 02110 page 49

Introduction to #MediGap

Our video explaining the Governments brochure on choosing a Medi Gap Policy. Click the little square on the right, to enlarge the video.

- 2025 Official Medicare Guide to choosing a Medi Gap Policy # 02110

- Spanish

- Get Quotes for Medi Gap Quotit

- Medicare Supplement Policies CA Insurance Code §§10192.1 - 10192.24

- CA Health Care Advocates HI CAP Fact Sheet

- If you have a Medigap policy and get care, Medicare will pay its share of the Medicare-approved amount for covered health care costs. In most Medigap policies, you agree to have the Medigap insurance company get your Part B claim information directly from Medicare. Then, your Medigap policy will pay your doctor whatever amount you owe under your policy and you’re responsible for any costs that are left. Learn More >>> Medicare.Gov

- Prior Authorization NOT Required! Askchapter.org *

- Supplementing Medicare: An Overview 10-30-20 Hi Cap

- Supplementing Medicare: Medigap Plans 12-14-23 Hi Cap

- Your Rights to Purchase a Medigap 12-14-23 HI Cap

- Search for Participating Doctors & Hospitals - Just about ALL of them!

- Anthem Blue Cross Information & Enrollment

- United Health Care

- Blue Shield – Medi-Gap Information & Enrollment

- Health Net

-

Medi Gap pays the medical expenses that Original Medicare Part A (Hospital) and Part B (Doctor) doesn't. Check out the chart on this page to see what Medicare Pays, what you pay and what a Medi Gap plan pays.

- If you have a Medigap policy and get care, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Then, your Medi-gap policy will pay its share. You’re responsible for any costs that are left. Medicare.Gov *

- More than half of all fee-for-service Medicare enrollees without any additional coverage chose a Medicare Supplement plan in 2021 Health Care Finance *

-

Original Medicare, Medicare Advantage nor Medi Gap pay for long term care either in a nursing home or at home care. Get more information on Long Term Care here.

-

Even if you think you can't afford any extra premiums, there's a lot of valuable information to help with planning.

-

Historical Information

& Reference

Insurance Companies cannot discriminate against

victims of #domestic abuse, regardless of sex. (Woods v Horton * Woods v Sherry pdf ) npr.org

CA Insurance Code § 10144.2

(a) No disability insurer covering hospital, medical, or surgical expenses shall deny, refuse to insure, refuse to renew, cancel, restrict, or otherwise terminate, exclude, or limit coverage or charge a different rate for the same coverage, on the basis that the applicant or insured person is, has been, or may be a victim of domestic violence.

(b) Nothing in this section shall prevent a disability insurer covering hospital, medical, or surgical expenses from underwriting coverage on the basis of the medical condition of an individual so long as the consideration of the condition

(1) does not take into account whether such an individual’s medical condition was caused by an act of domestic violence,

(2) is the same with respect to an applicant or insured who is not the subject of domestic violence as with an applicant or insured who is the subject of domestic violence, and

(3) does not violate any other act, regulation, or rule of law. The fact that an individual is, has been, or may be the subject of domestic violence shall not be considered a medical condition.

(c) As used in this section, “domestic violence” means domestic violence, as defined in Section 6211 of the Family Code. Abuse 6203 Definition

See also Health & Safety Code 1374.75

CA Insurance Code 676.9.

(a) This section applies to policies covered by Sections 675 and 675.5.

(b) No insurer issuing policies subject to this section shall deny or refuse to accept an application, refuse to insure, refuse to renew, cancel, restrict, or otherwise terminate, or charge a different rate for the same coverage, on the basis that the applicant or insured person is, has been, or may be, a victim of domestic violence.

(c) Nothing in this section shall prevent an insurer subject tothis section from taking any of the actions set forth in subdivision(b) on the basis of criteria not otherwise made invalid by thissection or any other act, regulation, or rule of law. If discrimination by an insurer is not in violation of this section butis based on any other criteria that are allowable by law, the fact that the applicant or insured is, has been, or may be the subject ofdomestic violence shall be irrelevant.

(d) For purposes of this section, information that indicates thata person is, has been, or may be a victim of domestic violence ispersonal information within the meaning of …Section 791)

(e) No insurer that issues policies subject to this section, and no person employed by or under contract with an insurer that issues policies subject to this section, shall request any information the insurer or person knows or reasonably should know relates to acts of domestic violence or an applicant’s or insured’s status as a victim of domestic violence, or make use of this information however obtained, except for the limited purpose of complying with legal obligations, verifying a person’s claim to be a subject of domestic violence, or cooperating with a victim of domestic violence in seeking protection from domestic violence or facilitating the treatment of a domestic violence-related medical condition. This subdivision does not prohibit an insurer from asking an applicant or insured about a property and casualty claim, even if the claim is related to domestic violence, or from using information there by obtained in evaluating and carrying out its rights and duties under the policy, to the extent otherwise permitted by this section and other applicable law.

(f) As used in this section, “domestic violence” means domestic violence as defined in Section 6211 of the Family Code.

FAQ’s

- Are you repealing patient protections, including for people with pre-existing conditions?

- No. Americans should never be denied coverage or charged more because of a pre-existing condition.

- We preserve vital patient protections, such as (1) prohibiting health insurers from denying coverage to patients based on pre-existing conditions, and (2) lifting lifetime caps on medical care. housegop.leadpages.co/healthcare

- ***

- Thus, the rest of this page is pretty much Historical

- Seniors & Medicare Supplements

Medicare Advantage Plans

Part D – Rx – Prescriptions - Waiving the Pre X Clause – Once I’m able to get coverage

- If I have prior medical insurance “Credible Coverage” and I get new health coverage will my pre-existing conditions be covered?

- If I do not have prior Credible Coverage will my pre-x be excluded forever, or just for say 6 months or a year

- What about the Pre X clause in visitor and travel policies?

- Claims Issues?

- What if something else makes the Pre-X worse, my pre-x causes a new problem, that is, how does the Insurance Company decide if the medical expense claim was from the Pre-X?

- What if I have say Hypertension – how would it be determined if that was the nexus or aggravation of say a Heart Attack?

- If I have a policy in force and then I get sick or develop a Pre – X can they cancel me or raise my rates?

- How can I appeal, complain or file a grievance?

- Does Obama’s Plan prohibit recessions Nationally?

- Misc.

- Where can I find Federal Regulations §146.111 or §2590.701-3 on Pre-X limitations?

- How will Obama’s Plan affect Pre-Existing Conditions?

- How do I get help if I’m not in California?

- Are there any Federal, State AB 88 or protections in Obama’s plan for Mental Illness?

- Underwriting

- In Individual plans Insurance Companies generally have the right to decide to give you a policy on not. This is called Underwriting.

- CA Department of Insurance Listing of typical Pre-existing conditions

- If there are any waiting periods in your new coverage, they are generally waived if 63 days of terminating your Insurance with another “creditable” health care plan.

- One Page – Pre Underwriting FORMS

- Do NOT miss your HIPAA 63 day deadline!

- When must a health plan write me?

- In CA under AB 1672 Small Employer Health Act §10705 j you can not be excluded as an employee or dependent in a group plan for health status. Employer group of 2 or more are guaranteed coverage.

- Mr. MIP Guaranteed coverage for individuals rejected from standard plans.

- Obama’s Interim High Risk Guaranteed Pool However, this plan just ran out of funding.

- Guaranteed Issue & Plans for Uninsured

- Federal Law 1182 – Group Plans must treat all similarly situated employees the same, regardless of health status.

- Steve, you’re website is the greatest, but I don’t live in California

- Guarantees for those who lost Employer Group Health Insurance

- COBRA and when that expires in 18 months or 36 months in California, then you can get a “HIPAA” policy

- How long is the Pre-X clause?

- In CA Group Plans, not more than 6 months 10198.7

- This clause can often be waived!

- Government Tools to help find coverage

- Case Law on Pre-Existing Conditions

- What if a don’t tell the Insurance Company about my medical history?

- Be sure to disclose whatever is asked for in the application, so that there isn’t a recession – cancellation later. Just because you paid cash or were treated by someone whose records are not available, doesn’t mean that just because it’s not on your “record” that it doesn’t count. In some cases, the Insurance Company will have your doctor verify your conditions on your first visit with your new coverage.

- Do NOT call or contact us in any way, if you plan to misrepresent yourself on an application for Insurance. We do not need the grief or the fine. We are mandated by law to certify that we do not know anything negative that is not on the application and that we explained to you how important it is to fill out an application correctly. We pride ourselves on helping the public get paid on LEGITIMATE claims and issues.

- Preexisting conditions, proximate cause

- When two causes join in causing injury, one of which is insured against, insured is covered by policy. Zimmerman v. Continental Life Ins. Co. (App. 1 Dist. 1929) 99 Cal.App. 723, 279 P. 464. Wiki Answers Ins.Code § 10320 exclusions must be listed in the policy itself.

- 10198.6. Preexisting Condition Provisions and Late Enrollees

10198.7. (a) - top

- Is one condition the nexus or aggravation of another? top

- Lastly, the veteran must have a nexus [connection] between the current disability and the in service disease injury or incident.

- In other words, there must be a link between the present disability and the veterans time during his period of active military service.

- There are many ways in which the veterans present disability can be connected to his disease, injury or incident in service. The VA is required to consider all the possible ways to disability could be service-connected.

- Probably the most common is direct service connection. This is when a disease, injury or incident in service directly caused the veteran’s present disability. These cases are usually won when you have a letter from a doctor stating that the in service disease, injury or incident was the cause of the veteran’s present disability. Because the veteran is given the benefit of the doubt a doctor only needs to be 50% sure that the in service condition caused the present disability. The language the VA accepts is that it is “at least as likely as not” that the veterans present disability is a result of the specified disease injury or incident in service. If the doctor uses the terminology that it is less likely than not he or she is saying they are less than 50% sure there is a connection. And if the doctor uses the terminology that “it is more likely than not” then he or she is saying there is a greater than 50% chance that the in service disease injury or incident caused the veterans present disability. These opinions from doctors are often called Nexus letters. If you are seeking a nexus opinion from your doctor it is extremely important the doctor is aware of the terminology used by the VA. It is also important for these opinion letters that the doctor have access to, review and state that he has reviewed your file and service medical records. If the doctor references the file in service medical records it strengthens the opinion even more. These opinion letters are even more important when you’re trying to prove service connection for a present condition many years after service.

- A veteran will have to show aggravation of a condition in service if the condition preexisted his service time. If the veteran can show his condition has worsened as a result of his time in service than the VA has the burden to prove that the worsening of the condition was due to “the natural progression of the disease.” One presumption in VA law that helps in these types of cases is the “presumption of soundness.” This means the veteran is presumed to be in sound condition when he entered service in less shown otherwise usually by the service entrance exam icdri.org/

- rbs law.com/

- veterans disability lawyer site.com

- Preexisting Condition Exclusions, Lifetime and Annual Limits, Rescissions, and Patient Protections

- Regulation

- Fact Sheet

- Patient Protection Model Notice

- Lifetime Limits Model Notice

- Public Comments

- With Guaranteed Issue Coverage coming 1.1.2014 many employees may leave their jobs to start new businesses. www.SteveShorr.com has been helping Small Biz with 2 or more employees in CA get guaranteed coverage since 1992 under AB 1672, Mr. Mip for individuals if they had no place else to go and HIPAA for those who have exhausted COBRA. We welcome NEW start ups. Free Individual Business Quotes

- It’s our opinion that under Health Care Reform that ONE employee business, even if it’s just the owner can get GROUP coverage. There is some dissenting opinion. We’ve sent a email to Covered CA for clarification.

- References

- ‘Employment Lock’ May Be Coming to an End

- Meanwhile, a new paper explores the phenomenon of “employment lock” — where workers stay in jobs they don’t like because of the health benefits — and concludes that given the new security of coverage expansion under the ACA, as many as 940,000 Americans will leave their jobs.

(CA Healthline)

-

-

No. The ObamaCare prohibition against Pre-Exisitng Conditions includes any limitation or exclusion.

-

Pre-Clause Waived if you had Prior Coverage

- If you apply for coverage within 63 days of terminating your membership with another “creditable” health care plan, then you can use your prior coverage for credit toward the six-month waiting period.

- CA Insurance Code for Small Group Plans 10708 c

- Individual Plans CA Insurance Codes §10198.6-10198.9 (might not be on point)

- Blue Shield FAQ’s PPO Share Brochure – Page 12

- Federal Guarantees HIPAA Health Insurance Portability and Accountability Act

What is a Pre Existing Condition?

- What medical issues might be considered Pre – Existing?

- What State or Federal Laws Define “Pre-Existing Condition?”

- What if I paid cash and there is no record of my illness or treatment?

- Does the Dept of Labor have a brochure to explain how HIPAA protects on Pre-X conditions?

- wikipedia.org

FAQ’s

Frequently Asked Questions

How can I get Affordable Individual or Family Coverage?

- Is there a simple ONE page form that I can fill out to see if my Medical conditions will still allow me to get Preferred Rates for Individual Coverage?

California Residents ONLY. - What about Guaranteed Issue plans, like:

Health Care Reform’s Pre-Existing Condition Plan

Mr. MIP or limited benefit plans like Get Med 360? - What about BMI and weight?

- What if I do not tell the Insurance company about my medical conditions?

- What if I was healthy when I filled out the application, but something happened later?

- Does the Government have any tools to help me find coverage?

- What about the new rule that kids under 19 cannot have a Pre X clause?

- What if I’m pregnant?

- What about Life Insurance?

State & Federal Laws that Define Pre-Existing Conditions

“Pre-existing condition provision” means a policy provision that excludes coverage for charges or expenses incurred during a specified period following the insured’s effective date of coverage, as to a condition for which medical advice, diagnosis, care, or treatment was recommended or received during a specified period immediately preceding the effective date of coverage. California Small Group Employer Plans AB 1672 CA Ins. Code §10700 (q) Appears to be exact same definition as in CA Ins. Code § 10198.6 c Federal Definition Title 42 300 gga wikipedia.org UHC Policy Extract

Pre X cannot include reasonable or prudent person would have sought treatment – Insurance Dept Bulletin 93.04 A

Also check the application for a definition of Pre X or what the health questions are.

19a. Within the last 2 years, have you had any serious illness or serious physical injury not mentioned elsewhere on this application that has not been evaluated by a licensed health practitioner?

19b. Within the last 2 years, have you visited a physician, psychiatrist, chiropractor, physician assistant, nurse practitioner, physical therapist or other licensed health practitioner that has not been disclosed elsewhere on this application? Blue Cross 3.2013 Application

CFR §146.111 Preexisting condition exclusions.

29 USC § 1182.

Prohibiting discrimination against individual participants and beneficiaries based on health status

(a) In eligibility to enroll

(1) In general

Subject to paragraph (2), a group health plan, and a health insurance issuer offering group health insurance coverage in connection with a group health plan, may not establish rules for eligibility (including continued eligibility) of any individual to enroll under the terms of the plan based on any of the following health status-related factors in relation to the individual or a dependent of the individual:

(A) Health status.

(B) Medical condition (including both physical and mental illnesses).

(C) Claims experience.

(D) Receipt of health care.

(E) Medical history.

(F) Genetic information.

(G) Evidence of insurability (including conditions arising out of acts of domestic violence).

(H) Disability.

(2) No application to benefits or exclusions

To the extent consistent with section 1181 of this title, paragraph (1) shall not be construed—

(A) to require a group health plan, or group health insurance coverage, to provide particular benefits other than those provided under the terms of such plan or coverage, or

(B) to prevent such a plan or coverage from establishing limitations or restrictions on the amount, level, extent, or nature of the benefits or coverage for similarly situated individuals enrolled in the plan or coverage.

(3) Construction

For purposes of paragraph (1), rules for eligibility to enroll under a plan include rules defining any applicable waiting periods for such enrollment.

(b) In premium contributions

(1) In general

A group health plan, and a health insurance issuer offering health insurance coverage in connection with a group health plan, may not require any individual (as a condition of enrollment or continued enrollment under the plan) to pay a premium or contribution which is greater than such premium or contribution for a similarly situated individual enrolled in the plan on the basis of any health status-related factor in relation to the individual or to an individual enrolled under the plan as a dependent of the individual.

(2) Construction

Nothing in paragraph (1) shall be construed—

(A) to restrict the amount that an employer may be charged for coverage under a group health plan; or

(B) to prevent a group health plan, and a health insurance issuer offering group health insurance coverage, from establishing premium discounts or rebates or modifying otherwise applicable copayments or deductibles in return for adherence to programs of health promotion and disease prevention.

Pre – X existing conditions deal with those medical problems that you’ve been treated for in the past or in some cases even a condition you’ve never been treated for, but know or should know that you have, paid cash or somehow think that it’s not on your record. The three main issues are:

- Can you get coverage?

- If you do get coverage, can and if so, for how long can the Insurance Company exclude coverage?

- If they can exclude coverage, must they cover you after a certain period of time and must they give you credit for time under your prior coverage?

- What about Health Care Reform and GUARANTEED Issue with no – pre X Clause?

See the FAQ’s below. If you are in California, email us a copy of your policy, application, etc. and we can help you. Not in CA?

Affordable Employer Group Coverage?

- Does AB 1672 in CA require Employer’s Group health plans, including if I start my own business have to write my coverage, and waive the Pre-existing Condition clause?

- Are there any rules or laws that say the Insurance Company must cover my Pre-X immediately if I pass underwriting or the Insurance Company is mandated to issue coverage to me? (employee in an Employer Group Plan, AB 1672, AB 1790)

- If I lost my coverage from my job, are there any guarantees?

COBRA

Cal COBRA

HIPAA When Cal Cobra is all used up.

Resources & Links

- Commonwealth Fund – Report ACA helped those with Pre X

- See Comments & FAQ’s below about the case pending in court to do away with this guarantee

- Jump to Pre ObamaCare Rules

- Donald Care vs Mandate & Keeping Pre X Clause Debate – Status – Fist Pounding

- AHCA Continous Coverage Requirement

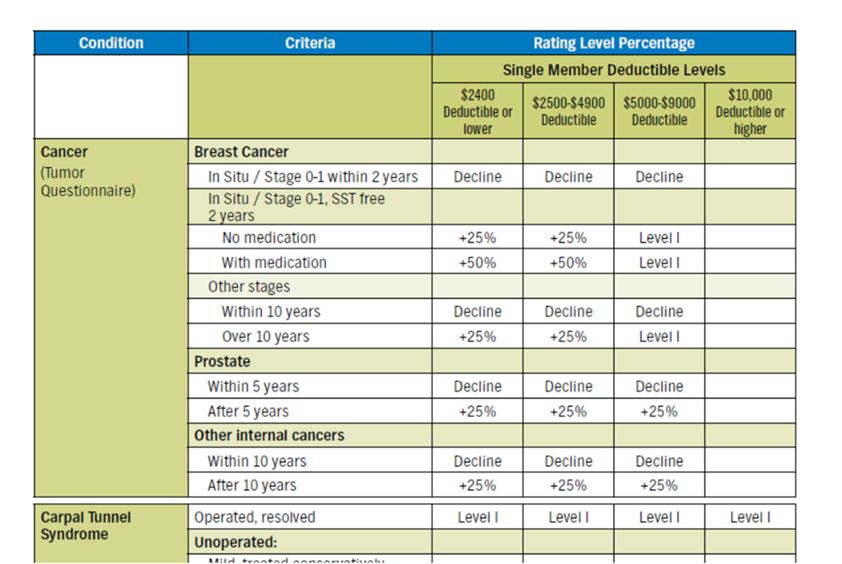

Cancer Underwriting

Sample Agent Guide

Pre ACA

Brother - Sister - Sibling Side Pages Subpages

View our website with your Desktop or Tablet for the most information

https://www.hhs.gov/civil-rights/for-individuals/section-1557/faqs/index.html